Why the Canadian Tech Scene Doesn't Work

Alex Danco's Newsletter, Season 3 Episode 1

Hello and happy new year! Welcome to Season 3 of the newsletter. I posted this week’s essay on my blog on Monday, and it’s safe to say it’s generated a fair amount of discussion since. I’m delighted to see these conversations happening, and look forward to what we’ll all get done together in 2021 and beyond. Thanks as always for reading and for keeping it interesting! -Alex

Toronto is not the next great startup scene. Neither is Waterloo, or Vancouver, or anywhere in Canada.

I’m sorry that I have to write this. I really am. I want it to work. But the growing chorus of aspirational claims that “Toronto’s tech ecosystem is growing faster than anywhere else in North America” or “The Toronto-Waterloo corridor is ’the nice person’s Silicon Valley’” honestly do not portray an accurate picture of what we’ve built here.

To be clear: I am not saying there are no individual success stories of Canadian startups, or that there are no good angel investors or VCs here, or that there are no individual instances of things going right. Shopify obviously worked out great, there are other big success stories like Lightspeed making their way up, we have some really good initiatives around bringing new builders into Canada, and there are a good many individually inspiring startups that I admire.

There is certainly a lot of something here. It’s true that big companies are adding tech jobs here; it’s true that there is a lot of activity in the startup scene here. But we do not have a real startup scene that actually works; not yet. You cannot put the Toronto tech scene side by side with the Bay Area’s and say, “These are similar; ours is just smaller.” Come on; it’s not. The Bay Area’s startup scene continuously pulls incredible companies into existence. Ours… does not do that.

The Canadian tech scene, as it currently operates, does not support startups. It stifles them. I’m sure for some of you it’s in your professional interest to insist otherwise, and look I respect that, but I care about us getting this right, and someone needs to say this so it might as well be me.

Angels

There’s no easy place to start. The startup scene is a system, with many interacting parts: Angel and VC money, the peer set of other founders, engineering talent, the set of social norms; everything depends on everything else. But we have to pick somewhere to start telling this story, and I think the best entry point is to talk about angel investors.

I remember back when I was at Social Capital, Jay and I would go visit other cities to check out local startups and university research facilities. Every time, we’d hear the same refrain from locals: “We’ve got so many great ingredients for a tech ecosystem here. We’ve got the science and hardcore R&D coming out of the local university system. We’ve got so much engineering talent. And there’s a lot of investment capital available. We’re just missing one thing, and that’s early stage investors.”

Well, yeah. A startup scene needs angels. Without a source of fast-moving, pre-institutional capital, it’s hard to pull off a cold-start when you’re first funding a project. But you know what’s even worse than no angel investors? Having bad angel investors.

In order to understand the difference between Good and Bad angels, I think it's helpful to have a quick understanding of Finite and Infinite Games, by James P Carse. This book introduces a simple but profound idea about there being two fundamental kinds of “games”, or multiplayer activities, that we engage in as people:

First, finite games are played for the purpose of winning. Whenever you’re engaging in an activity that’s definite, bounded, and where the game can be completed by mutual agreement of all the players, then that’s a finite game. Much of human activity is described in finite game metaphors: wars, politics, sports, whatever. When you’re playing finite games, each action you take is directed towards a pre-established goal, which is to win.

In contrast, infinite games are played for the purpose of continuing to play. You do not “win” infinite games; these are activities like learning, culture, community, or any exploration with no defined set of rules nor any pre-agreed-upon conditions for completion. The point of playing is to bring new players into the game, so they can play too. You never “win", the play just gets more and more rewarding.

Good Angels are playing an infinite game. They are contributing to a community; not in order to win something definite, but to earn the right to keep participating in the scene. They play the infinite game of growing their status within a growing community, which is a very good thing. And they often make a ton of money, leading to the perplexing advice for outsiders: “the way to make money angel investing is to not set out trying to make money.”

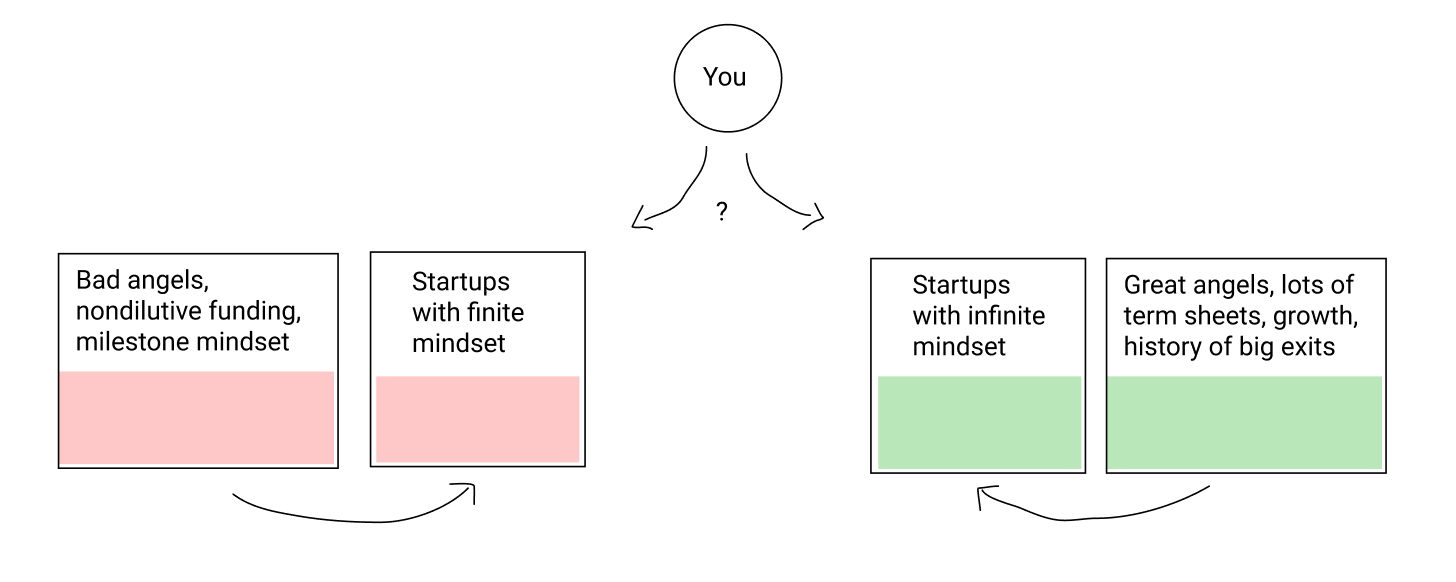

Bad Angels are playing a finite game. They are trying to win something.

There are two kinds of Bad Angels. The first kind are literally in it for the money: they want to see financial returns in a reasonable period of time, and push their founders to run their startups as an investment, like real estate. The second kind is more subtle: they’re Angels who’re doing it for the satisfaction and the status, but only among their own, closed peer set. They are competing for zero-sum bragging rights, not working to grow the community.

Bad angels waste founders’ time a lot. They’re always asking for something; either for P&Ls and business plans, or suggesting introductions that are clearly for the Angel’s social benefit rather than for the founder’s. Bad Angels care a lot about milestones. (More on this later.) You see these sorts of Angel investing clubs or societies on the east coast a lot. Canada has them too.

Good Angels have an entirely different attitude about the relationship between angels and founders. They’re not trying to win something; they’re trying to create something. This is a good thing, because that’s exactly the mindset you need to have, if you’re founding a startup. Startups are also infinite games. At the moment you found a startup, at no point in the next ten years (or whatever appropriately long time horizon) will you have “won” anything; nor is there a fixed set of rules you’re agreeing to. You are playing in order to keep playing. Your goal is growth, and growth is never done.

Of course, that’s not the only way to run a business. The majority of businesses can be appropriately described as finite games: you’re going after a bounded, definite opportunity; with a clear concept of what winning looks like. Canada loves these kinds of businesses; probably because our economy is made of banks and mines.

But these aren't startups, the way we use the term startups. Startups are a bet that the future will be radically different from the present, and they are valuable on the way up because they are, effectively, a call option on that future coming true. Their founders set out to discover that future; their value is indefinite, not definite. One day they might become giant, cash-gushing businesses; but not anywhere near your current horizon. Your only goal right now is grow, explore, and earn the right to keep growing and exploring.

So, as you might guess, there is a cross-catalytic relationship between Good and Bad Angels, and finite versus infinite-mindset founders. Each pair attracts each other, for obvious reasons. But just as importantly, the two kinds of angel investors mutually repel each other. If you have a critical mass of Good Angels, the bad ones will get pushed out (they’ll just stop getting invited to deals). And if you have a critical mass of Bad Angels, the good ones will leave (they won’t be having any fun, so they’ll go find a different hobby.)

If you have a background in electronics or in systems diagramming, you’ll recognize this setup: this is a toggle switch. It could break towards either side, but once it gets “set” on one side or another, it’ll tend to stay there.

So where do Good Angels come from? There is really only one reliable source of Good Angels, and that’s big liquidity events of other startups. Any other source of money is potentially suspect. But Angels who’ve made their starting nest egg from founding or growing a startup of their own understand the infinite game, because they’ve played it. And they want to keep playing it, because they like it, and Angel investing is how you do that.

Massive exits in a community have three really important feedback effects on next generation of startups. First, they create Angels, and motivate the existing ones with FOMO (nothing motivates you to invest more than having passed on eventual unicorns). Second, they inspire startups with the infinite mindset, as role models. Third, they set a high bar for what is possible, forcing the community to think about growth all the time, and releasing all of these operators back into the ecosystem who know what unbounded, indefinite growth feels like.

In contrast, in startup communities that haven’t had a lot of big exits yet, not only are you missing a few of those good ingredients, you also create one very bad ingredient and that’s a preoccupation with getting liquidity events. This is extremely dangerous, and the Canadian tech scene has fallen far down this trap. We’ll get back to this idea in a minute.

Deal Speed and Founder Leverage

The most visceral difference between the Canadian startup investing scene versus the Bay Area is speed. It is not an incremental difference: they operate on entirely different time scales. Bay Area startups can go from initially announcing their pre-seed round to closing an oversubscribed round of SAFE notes in 72 hours. In Canada, you’re generally lucky if you can get a deal done in 3 months.

Speed of deal completion is important on its own right (founders do better when they spend more time building and less time fundraising), and it’s also a good indicator for who has the leverage in the founder-investor relationship. In the Bay Area, it’s very clear who has the leverage; it’s founders. Deals get done quickly, cleanly, in-and-out; if an investor is a pain or slows things down inappropriately, they stop getting invited to deals.

There’s an interesting question here: in big startup ecosystems, why do deals happen faster and on more founder-friendly terms than in little startup ecosystems? It’s obvious that in ecosystems with more investors, they have to compete with one another. But there are also more startups. Why do more startups = more leverage for the startups?

The answer is actually pretty simple: the more startups in the scene, and the more deals happening in real time, the less time you have to think about any one deal - regardless of how many investors there are; it is solely a function of how many startups there are. And when you have very little time to evaluate each deal, you onlyhave time to ask: “what can go right.” And that’s a negotiation that’s on the startup’s terms. You only have to time to ask, who are the founders, how fast are they growing, and who’s investing. In other words, “Are you playing the infinite game, and will you get the runway to do it?” Those are the right questions to ask.

In contrast, in the Canadian startup ecosystem where fewer deals happen, there is more time to evaluate any one startup or any one deal. The world of startups is fully knowable, and there’s plenty of time, so the time spent on a deal will expand to fill the time available. And if there’s a lot of time available, then deal diligence will quickly enter determinate territory. You will find time to ask, “what can go wrong.” And you’ll find a lot!

This is bad, for two reasons. It’s bad because the very best startups, who have the longest time horizon and are most curious about the world, will look disproportionately uninspiring. They’ll have the fewest definite wins relative to their ambition, and the most things that can potentially go wrong. Paradoxically, you’ll also select away from the companies with the fastest growth rates, because fast growth rates (the best possible thing you can have as a startup) are not a definite accomplishment; you can always poke holes in them, you can always intellectualize reasons why the growth rate will stop. The longer you diligence a turbocharged growth rate, the more excuses you’ll find for why it can’t persist.

Conversely, it’s bad because startups will learn to optimize for how to get funded. So if seed deals take 3 months, then founders will learn to build companies that look good under that kind of microscope. And that means they’re going to optimize for playing determinate games, so that they can show definable wins that can’t be argued against; rather than what they should be focusing on, which is open-ended growth. (Canadian investors love to say, “Your growth is impressive, but we want to see some concrete milestones. We’ll fund you once you’ve achieved this definite accomplishment.” Startups listen.)

Unfortunately, in the long run, not only does this not select for the right startups, it undermines the startups’ own leverage. It’s a vicious cycle: the more that startups are selected for deterministic thinking, the more it ends up proving the VC’s skepticism right, and the less leverage the startups will have in negotiating terms next time around.

Even though startup ecosystem size & deal speed seem like continuous spectra, in reality it’s more like they operate in one of two modes: fast mode or slow mode. In fast mode, ecosystems like SF actually preferentially select for the startups that go on to do the most impressive things. In slow mode, ecosystems like Canada preferentially select for the startups working on the most determinate, measurable things. Just like the angel investing ecosystem can get “toggle switched” into either of two modes, same applies here: it’s not really a continuum. Once you get into one or the other mode, reinforcing loops take over. So it really matters which one you’re in.

Valuation and Milestones

Another fairly obvious difference between the Canadian startup ecosystem versus the Bay Area is that valuations are lower. It’s actually not just valuations that are lower; the price of everything is lower (including salaries, which is helpful if you’re staffing entry level positions but a huge problem when you’re trying to recruit experienced managers & senior talent). But the valuation issue is pretty central.

For a long time, Canadian VCs were effectively forbidden by their LPs to give out the rich, inflated, “indefensible" valuations that you saw in the Bay Area. (You spend how much of our money? At that valuation? For this?) In recent years, as it’s become clear to everyone that you actually need those high valuations to support a critical density of early-stage startup creation, that attitude has softened. But the “Canadian Discount” is still a very real thing.

In contrast, Canadian investors love to plan ahead for exits. You can’t blame them: they understand the value of these big liquidity events, and that we need more. They understand what we’ve been missing. It’s hard to overstate how much of the narrative around Canadian tech concerns: “we need to get more exits for the ecosystem.”

There is a Canadian Startup Inferiority Complex at work, and it compels us to defend our achievements: “Look at everything we’re doing! Look at these achievements, and look all these milestones our startups are achieving! Surely, these milestones are adding up to success.” We need a narrative that we’re on our way, that we don’t have these exits yet but we’re working on them; and that turns into a culture obsessed with milestones.

This preoccupation with milestones kills startups dead in their tracks.

Why are milestones so dangerous? Because when you define clear milestones, you initiate finite games: you’re defining and bounding the problem of startup-building, and inadvertently creating a “win/loss” condition upon the completion of the milestone. Just as before, when you start thinking in terms of milestones, you are no longer asking, “What can go right”, because you’ve already defined the boundaries of “right”. As soon as you start thinking in milestones, you enter the mindset of “what can go wrong”, and you actually break the special magic that makes VC work at all.

VC is a financial invention that’s been perfected to purchase call options on a different future, not in definably achieved milestones to date. The point of startups is to go through the J curve in an all-in bet on a belief about the future. When you are in the J curve, your “milestones” are not actually definable in a positive economic light; certainly not relative to capital raised.

I’ve written before about how “the greatest trick VCs ever pulled was calling it ‘valuation’”, and how the numbers on VC funding rounds are not actually pricing formally calculated valuations, they’re pricing discounts to the next round. Successfully funding a VC-backed company all the way through series C or whatever (at which point something resembling an actual valuation can take place) is essentially an exercise in rolling forward a “discount on a discount on a discount”: I’ll pay this $6M pre-seed valuation, not because there’s $6 million of tangible value here, but because it’s a discount to the next round (20), and then the next (50) and then the next (180). VC financing is a controlled bubble.

This method, as recursive as it sounds, is a legitimate financing innovation: it lets startups dig deeper into the J curve, repeatedly financing their business off of the possibility of “what could go right". But for it to work, you can never at any point formally value what’s been built. If you do, you puncture the bubble. (The exception is 409A valuations, which you want to be as low as possible. The sleight of hand with these, of course, is fantastic. Valuations are high and aspirational when we need them to be high, versus low and literal when we need them to be low.)

Our Canadian obsession with milestones, unwittingly, turns every startup financing event into something like a 409A valuation. Which is the exact opposite of what you want to do! This is a large part of why Canadian startups have lower valuations across the board than American ones; every time we define a “milestone”, we puncture the valuation bubble and then have to start again. Yet the investor community is continually compelled to do this (especially at early stage; what we’d call pre-seed and seed today), because of the need to show that we’re winning our finite, definable, “winnable” games.

Quite in character with our love of milestones, Canada loves anything with structure: accelerators, incubators, mentorship programs; anything that looks like an "entrepreneurship certificate”, we can’t get enough of it. We’re utterly addicted with trying to break down the problem of growing startups into bite-size chunks, thoughtfully defining what those chunks are, running a bunch of promising startups through them, and then coming out perplexed when it doesn’t seem to work.

Nondilutive Funding and Fancy Buildings

Hopefully by now you can see this picture coming together: the difference between the Canadian startup ecosystem versus the actually-functioning one in the Bay Area isn’t an incremental difference of degree. They’re two systems running in totally contrasting modes: one runs fast, rules opportunities in, rolls valuations forward, and is optimized for infinite-game-mindset founders. The other runs slow, rules opportunities out, feels the need to “defend” valuations (thereby collapsing them to their literal milestone value) and optimizes for fixed, finite games.

Unsurprisingly, the second one isn’t working. But it’s a priority of ours, on both a local and a national level, to somehow make it work. So we do the obvious thing: we add money.

One government program in Canada you may have heard of is called SR&ED credits (“Scientific Research & Experimental Development”), a government tax rebate program to encourage R&D spending by Canadian businesses. If you’re an established Canadian tech company, like let’s say Ubisoft, this program is totally helpful and as far as I can tell it’s a perfectly fine way for the government to subsidize technical employment.

But SR&ED credits also have a lot of appeal for startups. It’s “free money” to offset your R&D costs, and who doesn’t want that? So there’s a whole cottage industry in Canada around getting this money into the hands of startups, and helping them maximally leverage SR&ED as non-dilutive funding for technical work.

Unfortunately, SR&ED isn’t actually good for startups. It’s really unhealthy for them.

The problem with SR&ED credits, honestly through no fault of their own, is that you have to say what you’re doing with them. This seems like a pretty benign requirement; and honestly it’s pretty fair that a government program for giving out money should be allowed to ask what the money’s being used for. But in practice, once you take this money and you start filling out time sheets and documenting how your engineers are spending their day, and writing summaries of what kind of R&D value you’re creating, you are well down the path to destroying your startup and killing what makes it work.

The problem starts when founders think about SR&ED as “free money”. It is not free. It has a cost of capital, like any capital. But instead of costing you your equity, it costs you your time, your focus, and above all it costs you something you can never get back which is your indeterminate curiosity.

SR&ED forces you to play finite games, because it forces you to articulate what you’re spending this money on. And so you have to justify, at the very least, what problem you are solving and what specific steps you are taking to solve it. You enter the world of problem definition, where building your startup becomes Serious Work, with official time sheets and government forms.

The minute you take SR&ED money, some meaningful part of your startup becomes a government work program. And the minute any of your startup becomes a government program, I can pretty reliably tell you what’ll happen to the rest of it. By seeding an ecosystem full of SR&ED funded startups, the Canadian government inadvertently drained the spontaneity and curiosity out of our startup scene. It’s hard to recover from that.

Once you understand the problem of SR&ED credits, as well-minded as they are, you can easily understand by analogy what’s wrong with almost everything else the government does to support startups here in Canada too. We build spectacular buildings in downtown Toronto for hundreds of millions of dollars in order to “create space for the tech industry”, and then wonder why these startups suddenly become obsessed with doing all of the wrong things.

Meanwhile, we obsess over mentorship programs and other kinds of “non-dilutive help”, without realizing that there’s a cost to everything, including these relationships - and the steepest cost a founder can possibly pay is to give up an indeterminate trajectory. I mean, guess who these mentors are? They’re either people who have build successful Canadian businesses (finite games!) or, alternately, people from the tech industry who are signing up for formal mentorship programs rather than becoming angel investors. This is devastatingly expensive to startups; not only because these relationships consume the founders’ time, but because they helpfully impose “adult supervision” that robs founders of the very indeterminism that makes their companies valuable.

But because those costs aren’t easy to articulate, but the benefits can be easily tabulated and showcased, we just pile into them - and when the startup scene doesn’t seem to spontaneously self-organize into something like the Bay Area, we conclude, “Well, startups are hard, we need to support them more. Let’s build them some more buildings, and get them more grants!”

Terroir

So, let’s work our way backward through everything we’ve talked about here and understand how the Canadian startup scene has gotten stuck in the wrong way to do things.

Programs like SR&ED, Institutions like MaRS, and other well-meaning but disastrous government initiatives to support the startup ecosystem relentlessly pump money into the startup scene. This money is advertised as “free” or “non-dilutive”, but in reality it’s the most expensive kind of money you can imagine: it’s distracting, it begs justification, it kills creativity, and it turns your startup into a government work program.

Once your startup becomes a government work program, even if you pretend otherwise, you are forever onwards compelled to play fixed, finite games with your time and with your resources. You have to define what problem you are solving, and what you’re doing to solve it. You have to demonstrate value created.

The minute you spend any time doing that, with any part of your startup, that becomes the work product of more and more of the startup over time. Once you slip into playing fixed, definite games, that becomes everything you do. You become a milestone-oriented company, rather than a growth-oriented company. And there’s plenty of non dilutive money and government support for supporting and rewarding those milestones, so you can play this game for some time. So will your other founder peers, and this will just be normal.

But by becoming a milestone-oriented company, you’ve unwittingly destroyed your ability to actually put VC money to work, the way startups can do in California. And even before you take VC money, by becoming a milestone-oriented company, and learning how to talk and act in order to highlight those milestones and raise money off of them, you’re going to preferentially select for Bad Angels and disappoint Good Angels. The Good Angels simply won’t be having any fun: they won’t find the infinite game they’re looking to play, so they simply won’t play at all. So the early-stage funding environment gets saturated by the wrong type of money: well meaning, perhaps, but toxic to startups. And so startups start out hobbled, and likely never recover.

And this keeps the cycle going: the failure of these startups to sufficiently mature into unicorns (how can you blame them) compounds investors’ insecurity and obsession with “getting some exits for the ecosystem”, reaffirming their experience that these investments never generate any real returns, and reaffirming all of their decisions to say No rather than Yes. The ecosystem becomes defined and bounded by its small thinking.

And then, imagine you want to start a startup. Would you do it here? Or would you just get on a plane, and go to California?

Unfortunately, this decision compounds generation after generation of startups. For every batch of 10 new founders, the 2 most creative ones immediately leave (because it’s the right decision), leaving behind the other 8. They then start and grow their startups in this fixed-mindset, milestone-oriented environment, and become the environment that the next 10 founders step into as they graduate from Waterloo, or wherever. When the two particularly creative founders in that batch look around, yeah they’re probably gonna go to California too; again, leaving behind the other 8.

It was a bit of a bummer writing this essay. It’s not fun to write about this systemic trap we’ve gotten ourselves into; especially because there are so many individually good people and startups and firms in Canada who are trying their best to do good work. This is a system problem.

My hope is that people in Canada reading this will realize that the problem facing us isn’t a lack of anything. The problem with our startup scene isn’t a lack of money, startups, investors, hustle, great Universities, technical talent, or creativity. Our problem is actually the presence of actively bad things: all of our non-dilutive (but extremely expensive!) innovation credits, the presence of incubators and entrepreneurship programs, and the accidental costs of milestone thinking. If we want to build a real startup community in Canada, we need to let go of those crutches, and choose the Infinite Game.

That’s part of why I think that if any city in Canada has the potential to actually develop a Bay Area grade startup scene (smaller, sure, but actually the real thing), it’s clearly Montreal. Of the major cities in Canada, Montreal is the only one that naturally has an infinite game mindset. (But it really, really does. Montreal is a special place.) If Montreal weren’t in Quebec, it would be an unstoppable startup scene.

Anyway, I’ll wrap this up for now, but I hope we get this right eventually. In so many other ways beyond the tech scene, Canada is a special place. We’ve pulled off something absolutely incredible in our experiment of speedrunning multiculturalism; we’re (in my opinion) one of the overall nicest and freest places to live in the world; Canada is great and there’s a lot to be proud of here. But Canadian tech, specifically, can do better. I hope we do!

For other stuff to check out this week, first of all I don’t think I’ve actually talked about this on the newsletter yet - you have to check out what Patrick O’Shaughnessy and his team have put together in Colossus.

As you know, I’ve always been a long-time fan of Investor Field Guide and of its recent companion, Founders’ Field Guide. The amount of sheer knowledge and learning potential in there, in those episodes free for anyone to listen to, is just staggering. I don’t know how many times I’ve had the same conversation with people about how you could fill a world class MBA program 5x over with the free content in those episodes; the problem is just that it’s hard to access, trapped inside all that audio.

So, I’m just overjoyed (and also a little intimidated) with the drop of the next phase of that franchise, Colossus. Colossus is a learner’s dream come true. It’s an organized, searchable repository of all of the knowledge from all of Patrick’s guests, both founders and investors. If you haven’t yet, you need to go explore what’s in there.

Two recent episodes I encourage you to check out:

Ram Parameswaran of Octahedron Capital: internet-scale businesses

Carlos Cashman of Thrasio: Lessons from the Amazon ecosystem

And finally, this year’s inaugural Tweet of the Week, right after news dropped of the Plaid/Visa merger cancellation. Folks, it doesn’t get any better than this:

Have a great week,

Alex